Volume Weighted Moving Average (VWMA)

Volume Weighted Moving Average (VWMA) is a moving average in which each closing price is weighted by the trading volume of its candle. This means that high-activity periods have a greater influence on the indicator’s value than low-volume “quiet” candles.

Trend Identification with VWMA

Section titled “Trend Identification with VWMA”VWMA is used like other moving averages — by comparing it to the current closing price:

- Price above the VWMA line → buy signal (long).

- Price below the VWMA line → sell signal (short).

🔵 Thanks to volume weighting, VWMA more accurately reflects real market consensus: price moves backed by high trading interest shift the line more, while low-volume moves have little effect on its position.

VWMA Price Crossover

Section titled “VWMA Price Crossover”When the current price crosses the VWMA line, it may signal a local trend change:

- Crossover from above downward → signal to open a short position.

- Crossover from below upward → signal to open a long position.

The key value of VWMA crossovers is signal quality: if the breakout is accompanied by high volume, the move simultaneously shifts the VWMA line and confirms the strength of the trend.

Calculation Formula

Section titled “Calculation Formula”VWMA is calculated as the volume-weighted mean of closing prices over the last Length candles, where trading volumes serve as weights:

VWMA = Σ(Close[i] × Volume[i]) / Σ(Volume[i])

Where Close[i] is the closing price of candle i, Volume[i] is the trading volume of candle i, and the sum is taken over the last Length candles.

Timeframes and Practical Use

Section titled “Timeframes and Practical Use”- On liquid pairs with high trading volume, VWMA produces the most reliable signals — volume data is trustworthy there.

- On illiquid pairs or non-standard timeframes, volume data quality may be poor, reducing the accuracy of the indicator.

👉 VWMA works best in combination with momentum indicators (RSI, MACD) or volatility indicators (ATR). Use it as a signal quality filter, not as a standalone entry trigger.

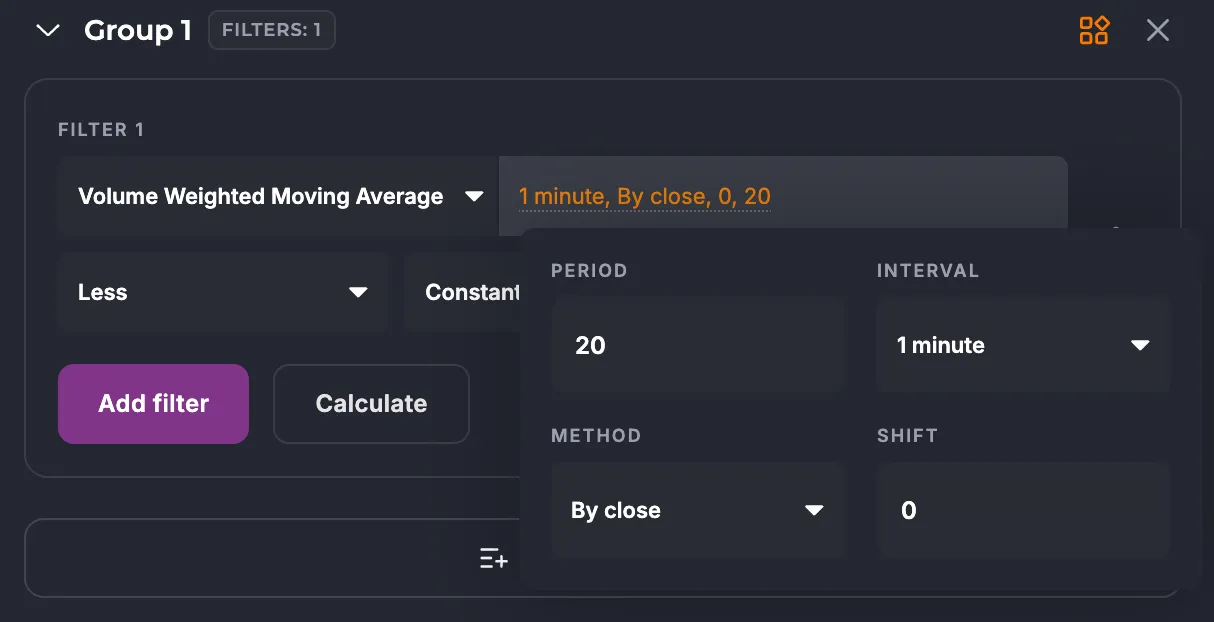

Use in Veles Bots (Flexible Indicators)

Section titled “Use in Veles Bots (Flexible Indicators)”Available settings:

- Period — number of candles for calculation. Range: 2–500, default value: 20.

- Interval — candle timeframe.

- Method — calculation type. By bar close (on the selected interval only), or by minute (once per minute for any interval).

- Shift — shifts the requested indicator value back by the specified number of candles.

Limitations

Section titled “Limitations”- VWMA is a trend indicator: it shows the direction of movement based on participant activity, but does not predict reversals.

- The indicator depends on volume data quality: on pairs with manipulated or unrepresentative volume, signals may be unreliable.

- For better accuracy, it is recommended to use VWMA in combination with other indicators (RSI, ATR, EMA) and support/resistance levels.

- In Veles bots, VWMA can be used as an entry or exit filter, combined with any other conditions.

Summary

Section titled “Summary”VWMA is a trend filter that accounts for real market activity when calculating the moving average. In Veles bots, it helps filter out entries on low-volume moves and build strategies based on market-participant-confirmed trends. Most effective on liquid pairs in combination with momentum indicators such as RSI or MACD.